This Company’s Shares Are Set to Benefit From the Auto Industry Revolution

Aptiv, which is helping make cars greener and smarter, is now undervalued and trading at a 24% discount.

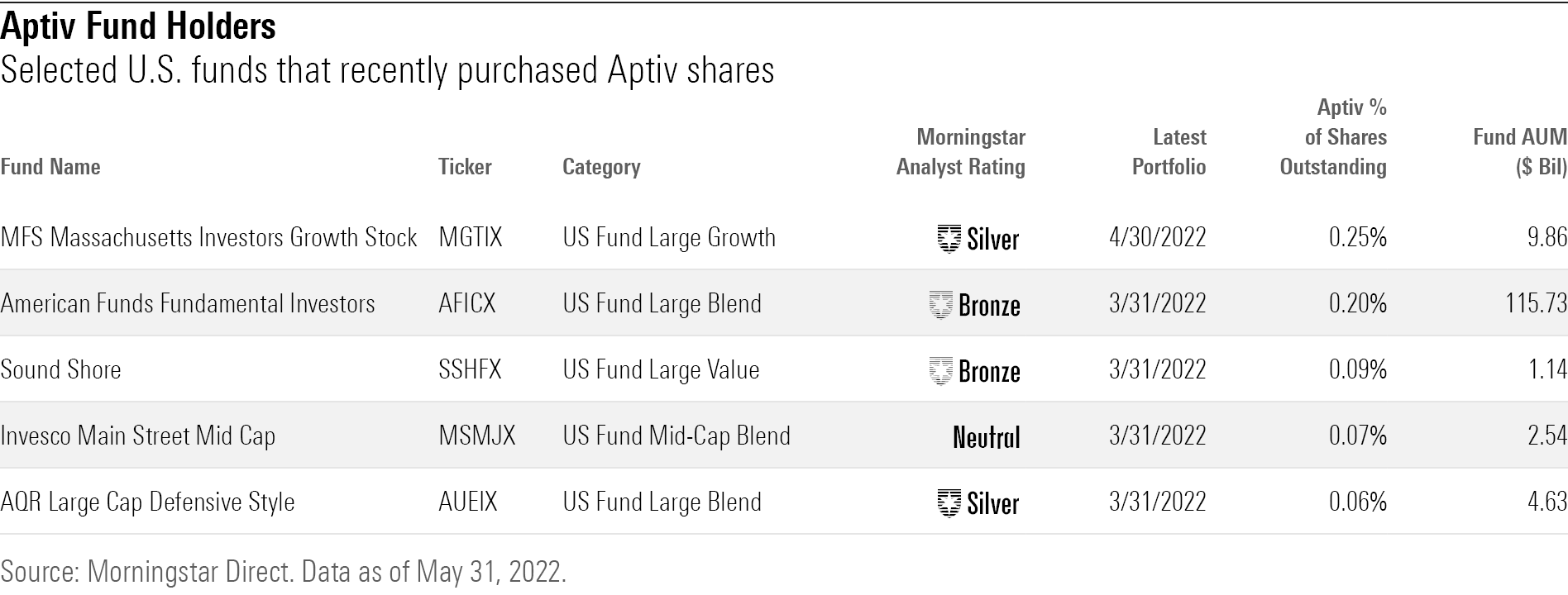

/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)

Every time you get into a car or truck there's a good chance you come into contact with a product made by Aptiv APTV.

It's Aptiv software that sends the alert when you're too close to another vehicle, and it powers the lane-departure radar that keeps you from drifting in front of, or into, another driver. And it is Aptiv that supplies the electrical distribution system and high-voltage connectors that help power your electric vehicle.

And yet at a recent price of $110, Aptiv’s stock trades at a 24% discount to Morningstar’s fair value estimate of $141 a share.

"When it comes to the stock, it's one of the best stories on the street," Morningstar senior equity analyst Richard Hilgert says. "Now is an opportune time for investors to be looking at Aptiv. It rarely trades below our fair value estimate and historically has always traded in 2-star range."

Hilgert puts Aptiv's average annual revenue growth at 12% a year between 2019 and 2026. Its earnings before interest, taxes, depreciation and amortization, or EBITDA, margin of 16.5 is one of the best in the sector. Aptiv's return on invested capital is in the high teens to low 20s and is also among the highest in the group.

"It has the highest growth rate of all the suppliers," Hilgert says.

Aptiv works with more than 20 global automakers and stands to benefit from the megatrends driving change in the industry as car- and truckmakers race to roll out the next generation of fleets that are greener, smarter, and safer. The good news for investors: While consumers are demanding these changes, many of them are the result of government mandates.

Morningstar Sustainalytics assigns a Low ESG Risk Rating to Aptiv based on environmental, social, and governance factors and considers it to have a low controversy level. The company holds wide appeal to those funds following ESG and impact strategies. Some of those with the biggest weightings of Aptiv shares in their portfolio are the UBS Engage for Impact UEIPX at 3.1%, BlackRock US Impact BIBFX at 3.4%, Cushing Global Clean Equity CGCNX at 2.9%, and Pax Global Opportunities PXGOX at 2.6%.

Undervalued Amid Improving Fundamentals

Hilgert assigns a narrow Morningstar Economic Moat Rating to Aptiv, noting a product pipeline filled with intellectual property and its ability to commercialize new technologies. He also points out that the company’s “sticky market share” is supported by deep relationships with customers and long-term contracts.

"We expect Aptiv's average yearly revenue growth to exceed average annual growth in global light-vehicle demand by 8 to 10 percentage points,” Hilgert notes. "Aptiv’s ability to regularly innovate and commercialize new technologies bolsters sales growth, margin, and return on investment.”

In mid-April, Aptiv was identified as one of 119 U.S.-listed companies considered to be undervalued in Morningstar’s coverage area of 866 firms that saw fair value increases of at least 10% based on improving fundamentals despite a difficult operating environment.

The stock is off its 52-week high of $180.81 and is down 37% year to date. Auto manufacturers and the parts and equipment sectors are among the worst-performing industry groups this year as supply chain woes, semiconductor shortages, and higher raw material costs have weighed on the entire industry.

Despite the challenges, Aptiv demonstrated its resilience in the first quarter when it reported earnings per share adjusted for special items of $0.63, beating the $0.61 estimate from Wall Street, according to FactSet. Still, earnings came in lower than the $1.17 per share for the prior year because of unpredictable customer production shutdowns, supply issues, and higher costs.

Exceeding Expectations

Aptiv’s first-quarter revenue also exceeded expectations, coming in at $4.18 billion, 4% higher than the year-earlier period. Revenue growth came in 11 percentage points higher than the 7% plunge in global light-vehicle production weighted to its customer base. Squeezed by lower production levels and inflationary pressures the operating margin of 7.8% was below the 11.8% reported a year ago.

An even brighter sign: Aptiv management stuck to its full-year 2022 sales outlook of $17.75 billion to $18.15 billion, earnings per share of $3.90 to $4.80, and an operating margin of 9.9% to 11.2%.

“They are benefiting from one of the strongest secular tailwinds,” says Quoc Tran, chairman and chief investment officer of San Rafael, California-based Tran Capital Management, which has $1.2 billion under management. He points to the rapid transition around the globe toward producing battery-powered electric vehicles.

Tran says Aptiv has content in one out of every 3.5 low-voltage vehicles and one out of every two battery-powered electric vehicles launched between 2020 and 2022. He notes that the dollar value for content in battery-powered electric vehicles is 2.5 times that of vehicles with traditional combustion engines.

The company’s planned $4.3 billion cash acquisition of Wind River from private equity firm TPG TPG, scheduled to close mid-2022, should also bolster its competitive position, especially with autonomous driving vehicles.

Is Aptiv a Good Stock to Buy?

Also adding to the potential value of Aptiv’s stock is Motional, its 50/50 autonomous driving joint venture with Hyundai HYU. Motional was formed for $4 billion in March 2020 and is now described by Tran as a hidden asset. Cruise, a self-driving car company backed by General Motors GM , among others, received a $30 billion valuation following its latest round of financing.

If Motional were to be similarly priced, that would put a value on Aptiv’s stake at $15 billion, more than half the company’s current market value.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZPLVG6CJDRCOTOCETIKVMINBWU.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)